Earnings Power. Strong quarterly earnings fuel global rally and reinforce the case for diversification.

KEY OBSERVATIONS

Markets rebound – Global equities rebounded sharply in April. Strong corporate earnings, led by mega-cap technology, restored investor confidence after a turbulent start to the year shaped by the conflict with Iran.

Diversification rewarded – Asset classes beyond U.S. large cap continued to pay. Emerging markets, international developed equities and U.S. small cap all delivered strong returns.

Fed keeps rates steady – The Federal Reserve held its policy rate at 3.50% to 3.75% as it weighed inflation pressure from higher energy prices against a softening labor market. April marked Chair Powell’s final FOMC meeting in that role.

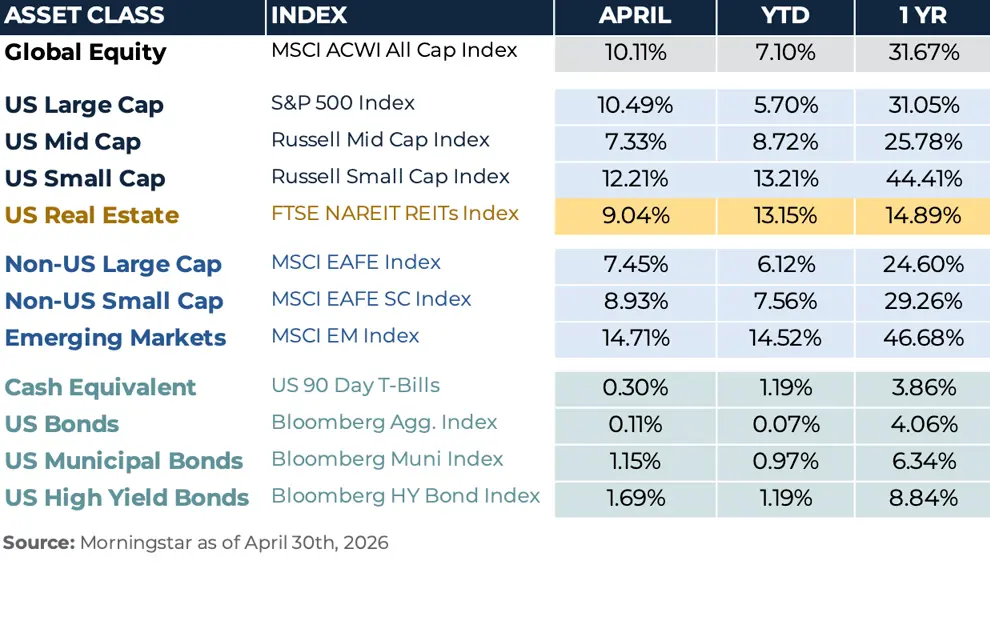

RECAP

April delivered a sharp recovery for global markets. After a difficult start to 2026 marked by the escalation of the Iran conflict and broader concerns about growth and inflation, investor sentiment shifted during corporate earnings season. Strong results, particularly from large U.S. technology companies, sparked a rally that pushed equities higher.

Large cap U.S. equities gained double digits, as the S&P 500 Index returned 10.5% for the month, supported by leadership from communication services, information technology and consumer discretionary. Positive earnings surprises from Alphabet, Amazon and Meta drove much of the upside. Smaller companies advanced even faster. The Russell 2000 Index gained 12.2% as easing recession concerns and improving earnings breadth across cyclicals supported a sharp rally. Information technology and industrials led the small-cap space, while energy and health care lagged. The FTSE NAREIT All Equity REITs Index gained 9.0%, with broad-based participation across property types. Office REITs jumped 13.6% on signs of stabilization in major metropolitan markets, and lodging, data centers and self-storage all rallied alongside improving fundamentals.

International equities also delivered strong returns. The MSCI EAFE Index rose 7.5%, with broad participation across Europe and Japan. Information technology, industrials and financials led the regional advance, while a weaker U.S. dollar amplified returns for U.S. investors and added more than 200 basis points to the index’s monthly gain. Emerging markets posted the strongest equity performance of the month. The MSCI EM Index climbed 14.7%, propelled by a 32.2% surge in the Information Technology sector as semiconductor and AI infrastructure demand continued to reaccelerate. Korea, Taiwan and India led individual markets, and the asset class is now up nearly 47% over the past year.

Fixed income produced more modest gains. The Bloomberg U.S. Aggregate Bond Index returned 0.1% as Treasury yields traded in a tight range but ultimately ended the month higher. The Federal Reserve held its policy rate at 3.50% to 3.75% at its April meeting, citing the need to assess the inflationary effects of higher energy prices alongside a cooling labor market. It was the third consecutive pause and Chair Powell’s final meeting in that role. Credit markets fared better. Spreads tightened on the back of the equity rally and stronger earnings, helping the Bloomberg U.S. Corporate High Yield Index advance 1.7%.

OUTLOOK

April reminded investors how quickly sentiment can shift when fundamentals reassert themselves. After a turbulent start to 2026, strong corporate earnings and easing tensions in the Middle East provided a powerful counterweight to macro headwinds earlier in the year and lifted nearly every major asset class. Diversifying away from U.S. large cap has been beneficial year to date, with small caps, international developed equities and emerging markets all leading. AI-related capital spending is broadening into more parts of the economy, and companies are delivering solid earnings growth. We will continue to monitor and should the situation evolve meaningfully we will follow up with the potential impact.