To the Moon (or Mars)? SpaceX IPO highlights the power of the AI narrative as enthusiasm continues to surround the broader ecosystem of companies viewed as enabling the next phase of technological growth.

KEY OBSERVATIONS

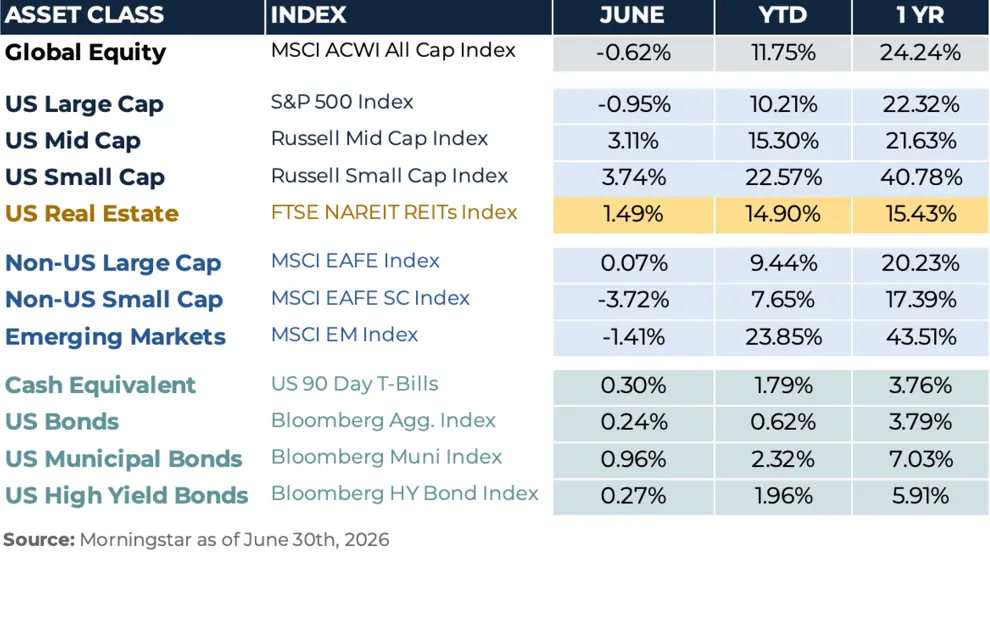

Passing the test – June offered a constructive test of portfolio diversification. Large cap U.S. stocks and emerging markets softened while small caps, developed market equities, and fixed income produced positive returns.

Ready for launch – The SpaceX IPO was a pivotal moment for private investor liquidity and the first in a growing pipeline of large cap IPO activity.

Healthy backdrop – Corporate fundamentals remain incredibly healthy but will be relied upon to continue supporting equity markets going forward as a flurry of new equity supply hits the market.

Mid-Year assessment – Strong first-half gains, especially in AI and technology, create an opportunity to revisit exposures, trim concentrated winners, and restore portfolio balance without necessarily reacting to losses.

RECAP

June brought an uneven tone to global markets as investors balanced still-resilient economic activity against sticky inflation, elevated geopolitical risk and a Federal Reserve that showed a desire to maintain a firmer policy stance. The month also marked a clear shift in market leadership. Large cap U.S. equities paused after a strong spring rally, while small caps, developed international equities and rate-sensitive real assets found support. The S&P 500 Index declined 1.0% in June but remained up 10.2% year-to-date, while the Russell 2000 Index gained 3.7%, extending its advance to 22.6% at the midway point for the year.

U.S. equity performance reflected a rotation beneath the surface. After several months in which mega-cap technology and AI-related enthusiasm drove much of the market’s advance, investors increased selectivity as inflation data and Fed messaging pushed back against hopes for near-term rate cuts. Small caps benefited from improved breadth, stronger cyclical participation and modest relief in bond yields late in the month. The result was a rare month in which the Russell 2000 meaningfully outpaced the S&P 500, reinforcing the notion that 2026’s equity gains are broadening beyond the largest U.S. companies.

International developed equities also posted solid results. The MSCI EAFE Index returned 3.1% in June and is now up 9.4% for the year, supported by broad participation across non-U.S. developed markets. Emerging markets moved in the opposite direction, with the MSCI EM Index declining 1.4% for the month, though it remains one of the strongest major asset classes in 2026 with a 23.9% year-to-date return. The divergence reflected a more cautious tone toward higher-valuation and geopolitically sensitive markets after a powerful early-year rally, particularly as investors weighed Middle East risks, energy market volatility and an uncertain global policy backdrop.

Fixed income returns were positive but muted. The Bloomberg U.S. Aggregate Bond Index gained 0.2% in June, while the Bloomberg U.S. Corporate High Yield Index returned 0.3%. The Fed held its policy rate steady at its June meeting, with Chair Kevin Warsh emphasizing price stability and removing some of the forward guidance that investors had grown accustomed to in prior cycles. That message landed against a complicated backdrop. May PCE inflation rose to 4.1% year-over-year while first-quarter GDP was revised higher to 2.1%, underscoring that the economy has not weakened enough to give the Fed a clear opening to cut rates. Credit markets were uneventful, with high yield supported by stable spreads and continued demand for income. Spreads remain very tight, reflecting a high level of optimism and little compensation for adding incremental risk to portfolios.

OUTLOOK

As we enter the second half of 2026, investors are presented with an opportune time to rebalance portfolios. Diversification shone during the first six months of the year, but those who were heavily allocated to the narrow themes of AI and technological innovation were not necessarily punished. This leaves a potential opportunity to reassess portfolio positioning and ensure proper balance in portfolios. For equity markets, the back half of 2026 will present challenges both new and old, including an increase in net equity supply, uncertainty surrounding monetary policy, and geopolitical risks. At the same time, corporate fundamentals remain supportive, and broader market participation could help reduce the dependence on a small group of mega-cap leaders. Fixed income also continues to offer a more compelling role than it has in much of the past decade, making it easier for investors to justify diversifying beyond equities. Elevated yields provide income, ballast, and a cushion against modest rate volatility, even as the Fed navigates a difficult mix of persistent inflation and uneven growth. In this environment, disciplined rebalancing, broad diversification, and a focus on long-term objectives remain the most reliable tools for managing uncertainty.