Global artery remains closed. March hands back the quarter's gains as the Strait of Hormuz stays shut and inflation anxiety returns.

KEY OBSERVATIONS

Markets collapse – In March Markets gave up much of the gains they had generated for the quarter as the Iranian conflict persisted. Stocks sold off on sentiment and rates rose based on inflation concerns.

Tech stocks pummeled – U.S. technology stocks, in particular software, pulled back the most as investors perceived advancements in artificial intelligence (or “A.I.”) as a threat to those business models.

Green shoots appear – The last day of the quarter ended with optimism that the U.S. and Iran will seek resolution sending markets notably higher. The motivation for de-escalation may be pressure on the homefront with midterms looming, but the robust economic backdrop is resilient enough to absorb the shock while resolution takes shape.

RECAP

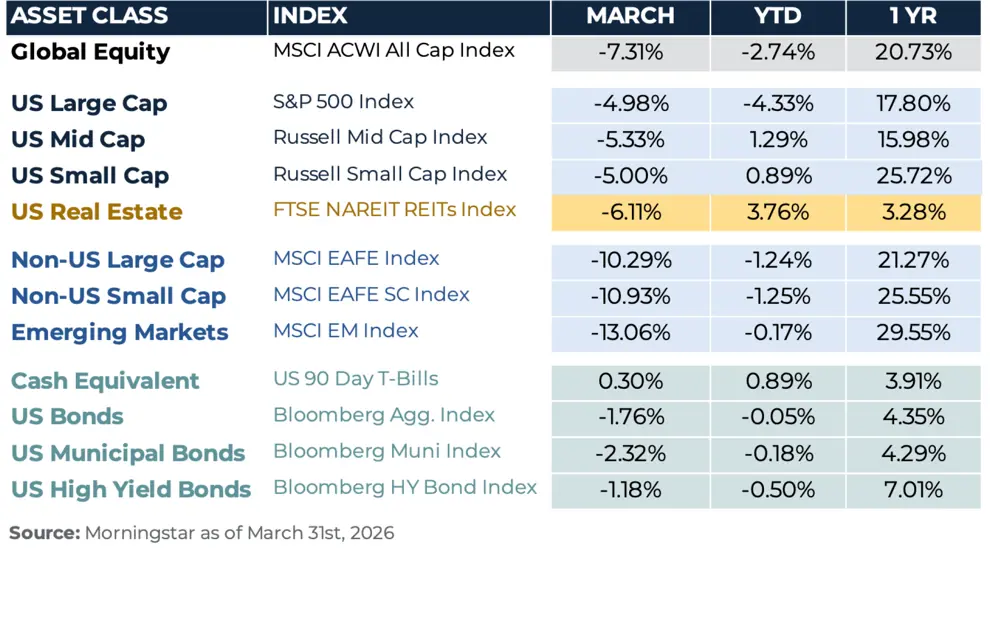

Global stocks retreated in March and the first quarter after a strong start in to begin the year. The S&P 500 ended the quarter down -4.3%, and the Nasdaq Composite fell -6.9%, marking their worst quarter since 2022. The Iran conflict dominated sentiment from its onset on February 28th. That said, the quarter closed on an encouraging note as green shoots of resolution emerged, and the S&P 500 surged +2.9% on March 31st, its best single trading day of 2026.

In the U.S., technology was the hardest-hit sector. Software stocks pulled back on concerns that AI investment would erode their competitive value. Over the last five years, software as a service traded at a 50% premium to the broader market. That premium has been erased over the last two quarters. The weakness drove a broad rotation into value stocks across every market-cap tier. Large-cap growth lost 9.8%, while large-cap value gained 2.1%. Small-cap value led all segments, rising 5%, as investors sought defensively positioned, attractively priced companies.

Outside the U.S., developed market stocks held up well by comparison, though March returns softened as the Iran conflict came into focus. For the quarter the MSCI EAFE fell just -1.2% and MSCI Emerging Markets slipped only -0.2%, both comfortably outpacing U.S. markets.

Bond markets offered modest stability. The Bloomberg U.S. Aggregate Bond Index was flat, TIPS rose +0.3%, and high yield bonds dipped just -0.5%, cushioned by income. Rates climbed through the quarter on inflation concerns tied to higher energy prices. Markets have largely erased expectations for a Fed cut in 2026, a sentiment we think may be overdone in the short-term.

WHAT WE’RE WATCHING

Two signals will define the long-term impact of this conflict. The first is whether Iran tests its leverage over the Strait of Hormuz. Before this conflict, the idea of an Iranian toll on commercial vessels was not a serious risk scenario. It is now. Nearly 140 ships transit the Strait each day. Iran has floated a $2 million levy per vessel. If implemented, that generates over $100 billion in annual revenue, nearly double its current oil export income of $53 billion. The financial incentive is real. A permanent toll regime would redirect global commodity flows toward China-aligned economies and create lasting friction for Western markets.

The second signal is the extent of damage to energy infrastructure. A swift resolution could reopen the Strait within weeks. But physical damage to production and refining facilities is a different problem. Repairs take months, sometimes years. If supply contracts structurally with no credible alternative to fill the gap, the inflationary pressure this conflict has already created may not resolve when the fighting does.

OUTLOOK

On balance, we see genuine reasons for measured optimism. Earnings growth is broadening, powered by A.I. and defense spending. The Bloomberg Economic Surprise Index sits near its highest level since 2023, and shelter costs, a stubborn driver of core inflation, continue to moderate. Critically, a soft labor market reduces pressure on the Fed to respond high inflation driven by energy prices. Collectively, these conditions buy time for a diplomatic resolution and create the backdrop under which one can succeed. The Suez Crisis (discussed in further detail here) resolved in weeks once political will collapsed under domestic pressure. We believe this conflict may follow a similar arc. The forcing function exists, the motivation is acute, and the economic backdrop remains resilient enough to absorb the shock while resolution takes shape. As a result we are maintaining current positioning and watching evolving conditions closely Risks remain, chiefly around infrastructure damage and Iran's willingness to negotiate in good faith, and we are watching both closely. Given the transitory and regionalized nature we described above, we believe portfolios are well positioned to navigate near-term volatility. We will continue to monitor and should the situation evolve meaningfully we will follow up with the potential impact.